Here's The Problem With TSP Lifecycle Funds

Here's The Problem With TSP Lifecycle Funds

When I first joined the military, in 2008, I chose to set up my TSP account as quickly as I could. Like many folks, I looked at the various funds available to me (without really understanding what any of them were) and chose the Lifecycle Fund that most closely mirrored my age, and expected retirement date. I set up my automatic draft, and promptly forgot about TSP altogether for the next year and a half.

Then, in 2010, I took Dave Ramsey’s Financial Peace University series of classes, and heard him recommend the 60/20/20 C/S/I strategy that I’ve talked about here before. So, I began to look more closely at TSP, and try to figure out why he would recommend that strategy versus the much simpler, much more hands-off, Lifecycle Funds. After all, I reasoned, wasn’t Dave all about “set it, and forget it” when it comes to investing? Shouldn’t he be a big proponent of target-date funds in general, and the Lifecycle Funds within TSP specifically?

Without getting into all the ways in which I now disagree with Mr. Ramsey, both personally and financially (that’s for another post), we can all admit that he’s generally considered a well-regarded financial advisor, particularly among conservative folks like the ones who generally make up the military. Why would he choose to avoid recommending TSP’s Lifecycle Funds, I wondered? That led me to realize that we have to first understand what the Lifecycle Funds, and other target-date funds, are designed to be and do.

According to Investopedia.com, target-date funds (which is what the Lifecycle TSP Funds are) exist to “grow assets in a way that is optimized for a specific time frame.” Therefore, while most target-date funds are IRA vehicles geared toward a notional retirement date, there are target-date funds for virtually any timeframe. There are 529 college plans that are geared toward target-date funds. There are a multitude of other time horizons, all geared toward achieving a specific monetary outcome within a specific amount of time.

Managers of target-date funds use the time horizon of their specific fund (whether a few years, or several decades in the case of some retirement funds) to calculate risk and make investing decisions. Generally speaking, the “younger” a target-date fund, the more risk and potential for loss its managers will tolerate. As the fund matures, and the target-date draws closer, management is supposed to shift to more stable, less volatile investment strategies focused on preservation of capital. An easy example would be a target date fund that is split between stocks and bonds. Initially, the fund should be made up of a high percentage of stock shares, and a lower percentage of bond shares. As the fund matures, that ratio should swing the other way until, at the maturity date (the “target date” of target-date funds) the money should be invested almost exclusively in bonds and other stable, secure instruments.

A target-date fund can be an excellent “set it and forget it” method of investing, simply because you, as the individual investor, don’t have to remember to rebalance your portfolio as you age. You also don’t have to know anything about the market, or about buying or selling shares, or really anything at all about investing other than how to set up a direct deposit. As your fund matures, and you age, you can rest assured that the smart financial managers working in the background of your fund are making the right decisions at the right time, to ensure maximum value for you.

The other essential component of target-date funds is preservation of capital. They are inherently lower risk (and consequently lower in performance) than index funds, passive ETFs, and other non-retirement funds. Consequently, you shouldn’t expect to see the same return on investment in a target date fund that you will see in an index fund. However, you should expect that a good target-date fund will be the most aggressive (read: heaviest in stocks) at the beginning of its life, and gradually transition to more stable, less risky, things like bonds as it matures. So far, all well and good. The problem comes when we compare the TSP target-date funds to their peers in the civilian sector.

The simple fact is that the TSP Lifecycle Funds are unnecessarily conservative, by which I mean that the risk avoidance in down years doesn’t make up for the lack of performance in up years. Military investors who want to utilize a target-date fund need to understand how much money they are potentially leaving on the table if they use the TSP L funds instead of a similar product from a commercial provider.

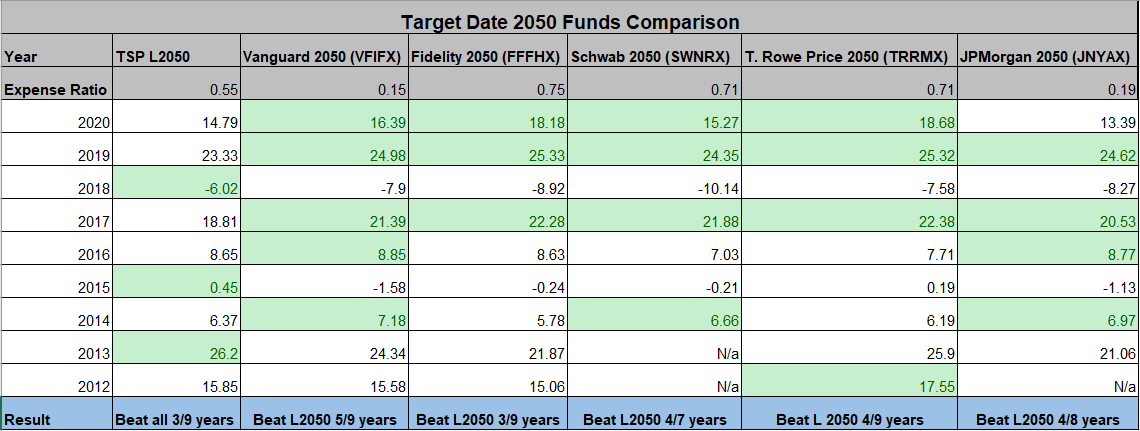

Based on my current age, my most likely date of retirement would put me in line with TSP’s Lifecycle 2050 fund. So, I created a chart that lists the year-on-year ROI since inception of the TSP L2050 and compares it with 2050 Target-Date Funds from five other well-known companies including Vanguard, Fidelity and T. Rowe Price:

As we can see, there are only three years of the past nine (2013, 2015, 2018) where the TSP fund has outperformed its peers. And, in fact, the Vanguard and JPMorgan Funds not only outperformed TSP more than 50% of the time, but they have significantly lower expense ratios as well!

In a further effort to compare the funds and see if there was some metric by which the TSP fund came out ahead, I compared 5 year returns. The numbers there were even more stark:

VFIFX 5 yr return: 14.69%

FFFHX: 15.63%

TRRMX: 15.68%

LIPKX: 14.89%

SWNRX: 14.01%

TSP L2050: 11.9%

And that, in a nutshell, is the problem with the Lifecycle Funds. While we would expect target-date funds to be growing gradually more conservative as time goes by, and the fund seeks preservation of capital, there’s no justification for the TSP funds to significantly underperform the rest of their peers, and sacrifice the extra growth, particularly in the early years.

If you want a true “set it and forget it” option that frees you up from having anything to do with your retirement other than remembering to make your contributions monthly, you’d be much better off, and much wealthier on the day you retire, if you chose a target-date fund from a commercial investment company, rather than the Lifecycle Funds offered in TSP.

Thanks so much for reading! Please don’t hesitate to let me know what you think in the comments, and if you want to keep in touch, and never miss another post, consider clicking the subscribe button below!